What is this option strategy?

The Double Diagonal option strategy is a two-legged spread, calling for the simultaneous purchase and sale of two separate options; a short-term call and long-term put option. The call and put options are both of the same type and contract size. In this strategy, the trader is looking for a stock to stay within a predetermined range for the length of the option’s expiration.

Is this a Bullish or a Bearish strategy?

The Double Diagonal option strategy is generally considered a neutral to slightly bullish strategy as the trader is attempting to profit from the stock remaining in a range as opposed to explosive price movements in either direction.

Is this a beginner or an advanced option strategy?

The Double Diagonal option strategy is considered an advanced option strategy, as it requires a trader to have a thorough understanding of both stock and options trading. Although the strategy is neutral to slightly bullish, a trader must understand the various factors that can move the stock price and how to adjust the strategy in order to make a profit.

In what situation will I use this strategy?

The Double Diagonal option strategy is often used when the trader believes that a stock or index will remain in a tight price range for the duration of the options contracts, or when the trader is expecting only a small price swing in the near-term.

Where does this strategy typically fall on the risk-reward vs probability of profit continuum?

The Double Diagonal option strategy typically carries moderate risk, with a potential reward that can be better than the risk taken. The probability of a successful outcome depends on a variety of factors, such as the current stock price, the type of options traded, the strike price, and the duration of the options.

How is this strategy affected by the greeks?

The Double Diagonal option strategy is affected by the Greeks—the risk measures such as Delta, Gamma, and Theta. Delta measures the extent to which change in the underlying stock affects the price of the options. Gamma measures the exposure to the underlying stock. The Theta measures the effect of the passage of time on the options.

How do you adjust this strategy when the trade goes bad?

When the trade goes bad, the trader can adjust the Double Diagonal option strategy by either closing the existing position and taking the loss, or adjusting the strategy by buying or selling more options to create a different position. The goal of the adjustment is to turn the position into a profitable one.

How do I know when to exit this strategy?

The trader should exit the Double Diagonal option strategy when the trade is no longer moving in the desired direction. That is, when the stock’s price moves above or below the predetermined range, the trader should exit the position in order to limit potential losses and maximize potential profits.

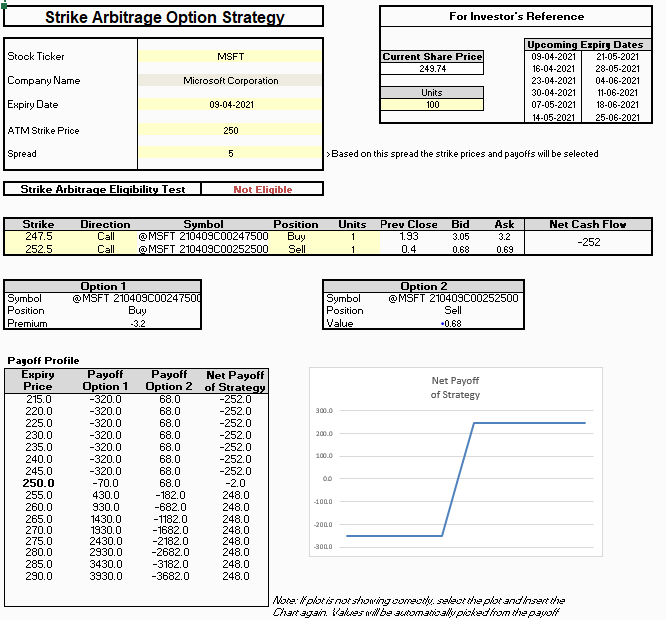

Describe an example of this strategy and give me the p&l data in a python dictionary to create a chart. Use MSFT as example and assume current price is 150, On x axis I need the price and on y axis I need the profit.

For example, using Microsoft (MSFT) at a current share price of $150, the trader purchases one out-of-the-money call option (with a strike price of $152.50) and sells one out-of-the-money put option (with a strike price of $147.50). The call and put options both expire 45 days from now. If Microsoft does not break outside of the predetermined range of $147.50 to $152.50, the trader may make a profit on their position. Here is the expected profit and loss over various MSFT stock prices, expressed in a Python dictionary:

“`python

pnl = {

134: -16.00,

135: -15.00,

136: -14.00,

137: -13.00,

138: -12.00,

139: -11.00,

140: -10.00,

141: -9.00,

142: -8.00,

143: -7.00,

144: -6.00,

145: -5.00,

146: -4.00,

147: -3.00

Here are some templates that you can use to create your own models

Search for all Templates here: https://marketxls.com/templates/

Relevant blogs that you can read to learn more about the topic

Double Diagonal Option Strategy

Leverage Vega to Maximize Your Option Gains