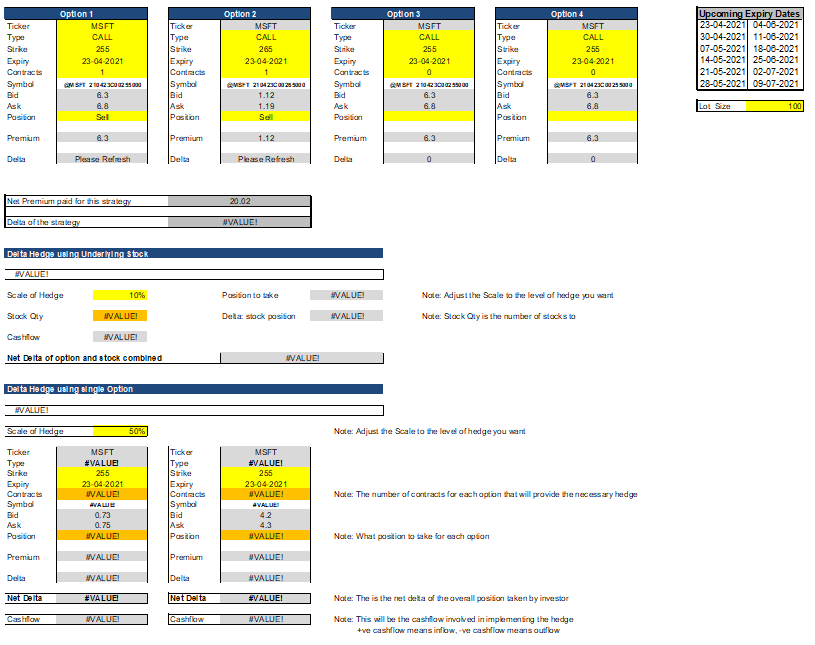

The Delta Neutral Hedging strategy is for the investors who want to reduce the delta of the overall option strategy. It can be done using the underlying stock or using an option. The idea is to reduce the payoff movement per dollar change in the underlying. The traders use delta-neutral hedging to reduce the exposure in the event the position moves against them. The flip side is that the risk comes at a cost of reduced profit potential.

In the active file, the user can input the option strategy he wants to implement using the four option boxes provided.> User has to enter the ticker, expiry, strike, and a number of contracts for each option involved in the strategy.> The system will calculate the Delta of the strategy and also the total premium to be paid.> If the delta of the overall strategy seems high, he can reduce it in two ways. Using Stock or using options. Both the methods have been implemented in the below sections on the active file.> User is enabled to enter the level of hedging he wants against the prior delta of the strategy and the template will recommend the appropriate action to take to reduce the overall delta.

For the stock, the template will highlight the position to take on the same underlying and the number of stocks along with the cash flow involved.

The Option, the template will show both the Call and Put options that can be used to reduce the delta and it is up to the user’s discretion to use whichever option he wants. The system will assist by showing the cash flow involved and also the final delta of the positions.