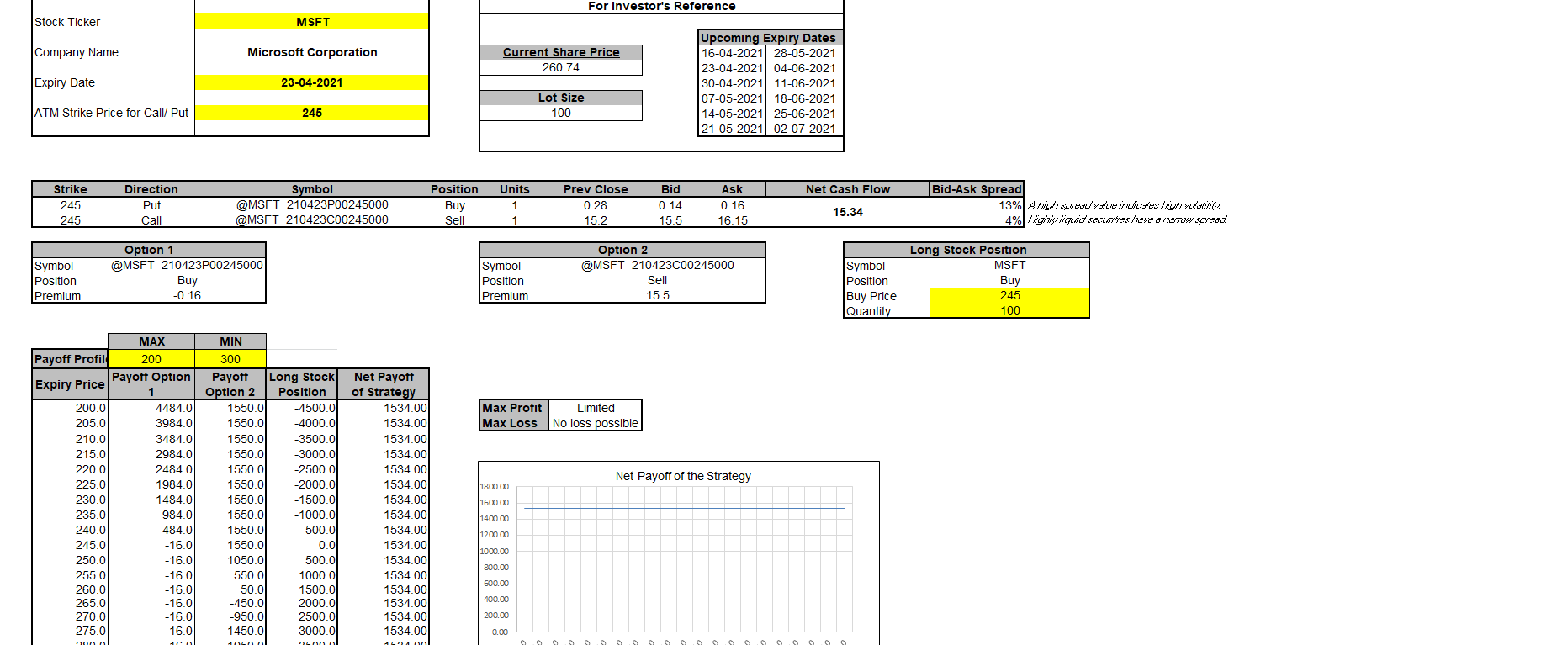

A conversion is an arbitrage strategy in options trading that can be performed for a riskless profit when options are overpriced relative to the underlying stock. To do a conversion, the trader buys the underlying stock and offset it with an equivalent synthetic short stock (long put + short call) position i.e. buying 100 shares, buying 1 ATM Put and selling 1 ATM Call with identical strike prices and expiration dates.

This strategy is employed to exploit perceived inefficiencies that may exist in the pricing of options for a riskless profit. To implement this strategy, the trader buys the the underlying stock and simultaneously offset that trade with an equivalent synthetic short stock position (long put + short call). The long stock position carries a positive 100 delta, while the synthetic short stock position using options has a negative 100 delta, making the strategy delta neutral, or insensitive to the direction of the market.