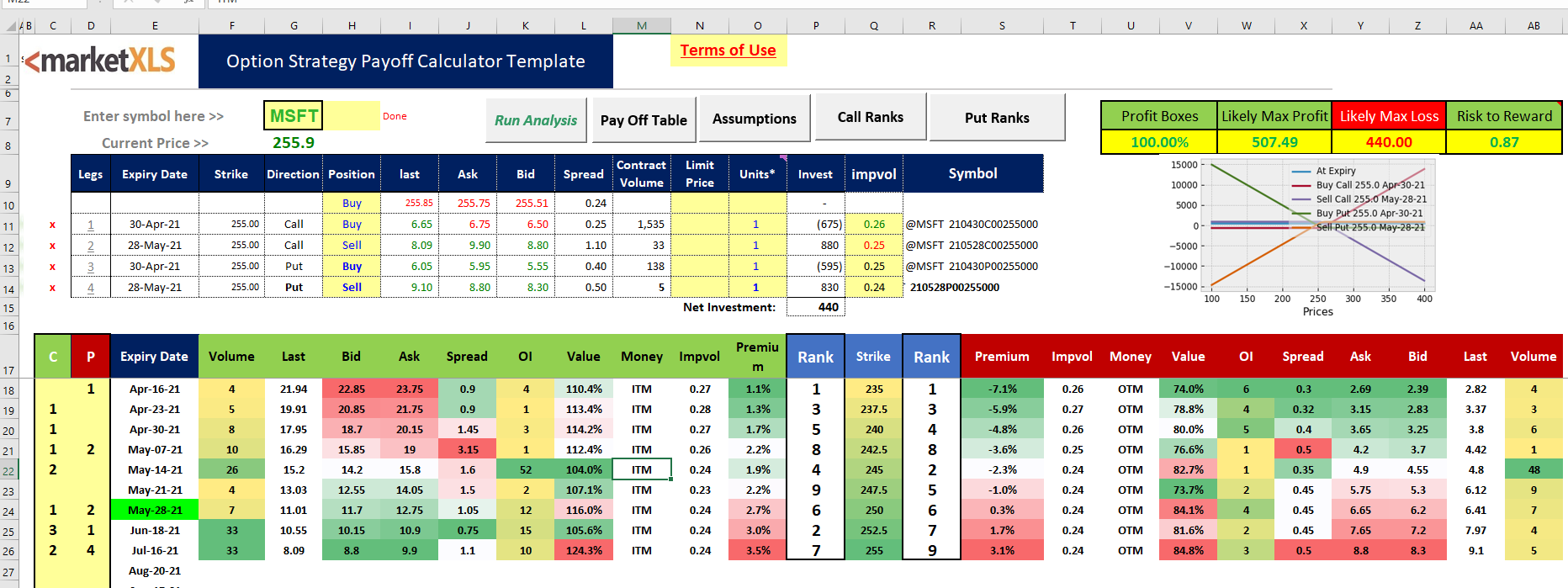

The Calendar Straddle is a neutral options strategy designed to profit when a stock is expected to moved within a tight channel in the short term while still keeping the potential for profiting should the stock stage a breakout. The Calendar Straddle produces this effect by buying a long term straddle while writing a short term straddle.

It can be implemented by selling a near term straddle while buying a longer term straddle with the intention to profit from the rapid time decay of the near term options sold. It is a limited profit, limited risk strategy entered by the options trader who thinks that the underlying stock price will experience very little volatility in the near term.