The option premium is described in this article and calculated by the Options Profit Calculator with MarketXLS. Option premium depends on different variables, which are listed in detail. This article will discuss how to calculate the option premium of your portfolio.

Contents

- What is Option Premium?

- Impact of Option Greeks on Option Premium Pricing

- Option Pricing Calculation

- Option Pricing Models with MarketXLS

What is Option Premium?

An option premium is a price that traders pay for a put or call options contract. When you buy an option, you’re getting the right and not an obligation to buy or sell the underlying asset like a stock, securities, commodities, etc. at a specified price for a defined future date. The price you pay for this right is called the option premium.

Three main factors influence the size of an option’s premium: the price of the underlying market, it’s level of volatility (or risk), and the option’s time to expiry.

The option premium is continually changing. It depends on the price of the underlying asset and the amount of time left in the contract. The deeper a contract is in the money, the more the premium rises. Conversely, if the option loses intrinsic value or goes further out of the capital, the premium falls.

Impact of Option Greeks on Option Premium Pricing

The option premium is affected by factors like the underlying asset’s price, the volatility of the underlying, term to maturity, and the risk-free rate. Any change in these factors would impact the option price.

These metrics are often referred to by their Greek letter and collectively as the Greeks. Options Greeks are a group of notations which define the sensitivity of the factors on the option price.

Option Greeks are various factors which help option trader in trading options. The following are the different Option Greeks in the market:

Delta (Δ) – It calculates the extent to which option premium would change because of a small change in the underlying price. Delta measures the difference in the value of premium to change in the value of underlying. For a call option, Delta’s value varies between 0 and 1, and for a Put option, the value of Delta varies between -1 and 0.

Gamma (Γ)– It calculates the extent to which Delta would change because of the change in the underlying value. It defines the speed with which option would become in-the-money or out-of-the-money due to fluctuations in the underlying price.

Theta (Θ) – Theta is an essential factor in deciding option pricing. Time is an ingredient in determining the premium for a particular strike price. Time decay reduces the option Premium as it nears expiry. Theta is the time decay factor, i.e., the rate at which option premium loses value over time as it is near expiry.

Vega (v) – Vega, as a greek, is sensitive to the current volatility. Volatility is the rate of change because of the changes in market volatility. Vega signifies the difference in the value of an option for a 1% change in the underlying asset price. Higher the volatility of the underlying asset, the more expensive it is to buy the option and vice versa for lower volatility.

Rho (p) – Rho is a metric used for assessing the sensitivity of an option premium to changes in the risk-free interest rate. It is expressed as the amount of money an option will lose or gain with a 1% change in interest rates.

Option Pricing Calculation

Several factors determine the value of the premium – the underlying stock price relating to the strike price (intrinsic value), the length of time until the option expires (time value), and how much the price fluctuates (volatility value).

Market price, volatility, and time remaining are the primary forces determining the premium. There are two components to the options premium, and they are intrinsic value and time value. Option premiums are calculated by adding an option’s intrinsic value to its time value.

Premium = Time Value + Intrinsic Value

The intrinsic value is determined by the difference between the current trading price and the strike price. Only in-the-money options have intrinsic value. Intrinsic value can be computed for in-the-money options by taking the difference between the strike price and the current trading price. Out-of-the-money options have no intrinsic value.

The time value is dependent upon the length of time remaining to exercise the option. The time value of an option decreases as its expiration date approaches and becomes worthless after that date. This phenomenon is known as time decay.

For in-the-money options, time value can be calculated by subtracting the intrinsic value from the option price. Time value decreases as the option goes deeper into the money. For out-of-the-money options, since there is zero intrinsic value, time value = option price.

Option Pricing Models

The option pricing model uses variables such as stock price, exercise price, volatility, interest rate, time to expiration, to theoretically value an option. Essentially, it provides an estimation of an option’s premium value, which traders incorporate into their strategies to maximize profits.

The option pricing model’s primary goal is to calculate the probability that an option will be exercised or be in-the-money (ITM) at expiration. Some commonly used models to value options are Black-Scholes, binomial option pricing, and Monte-Carlo simulation.

Black- Scholes Model

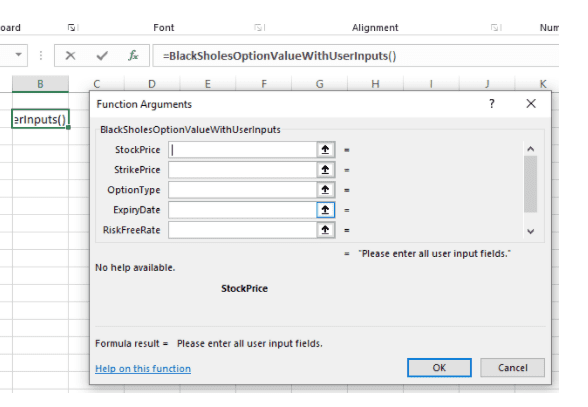

Black-Scholes is a pricing model used to determine the fair option premium price for a call or a put option based on variables such as volatility, type of option, underlying stock price, time, strike price, and the risk-free rate.

The quantum of speculation is more in stock market derivatives, and hence proper pricing of options eliminates the opportunity for any arbitrage. The model assumes stock prices follow a log-normal distribution because asset prices cannot be negative (they are bounded by zero).

According to the Black-Scholes model, the assumption of log-normal underlying asset prices should thus show that implied volatility are similar for each strike price. The model is used to determine the price of a European call option, which means that it can only be exercised on the expiration date.

Binomial Pricing Model

The Binomial Options Pricing Model provides investors with a tool to help evaluate stock options. The model uses multiple periods to value the option. The model simulates the options premium at two possibilities of price movement (up or down). The periods create a binomial tree — In the tree, each tree shows the two possible outcomes or the price movement.

The model creates a binomial distribution of possible stock prices for the option. It creates possible paths that the stock price could go until the expiration date and the resulting impact on the options premium.

The Binomial options pricing model calculates the price of the option at various periods until the expiry. A binomial tree is a useful tool when pricing American options and embedded options.

Monte-Carlo Simulation Model

Monte-Carlo simulation involves creating random variables. These variables have similar properties to the risk factors which the simulation is attempting to simulate. Monte-Carlo simulation simulates and produces several outcomes for many scenarios over a large number of time-steps.

As a result, the technique produces many possible outcomes of variables, along with their probabilities. Monte-Carlo simulation can be used to mimic real-life scenarios and generate outliers. From the possible outcomes of the values, an average value is chosen. The average measure is usually dependent on the use case.

The larger the number of scenarios, the higher the accuracy of the results, but the slower the simulation’s computation. Monte-Carlo valuation works as it can be used to price more complicated trades such as the American call option, which can be expired earlier than the time to expiration.

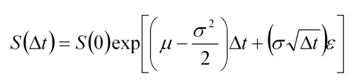

Calculation

The first step in using Monte-Carlo methods is to generate a large number of potential future asset prices. It is done by selecting an appropriate stochastic model for the time evolution of the underlying asset(s) and then simulating it through time.

where,

S(0): The stock price today.

S(Δt): The stock price at a (small) time into the future.

Δt: A small increment of time.

μ: The expected return.

σ: The expected volatility.

ε: A (random) number sampled from a standard normal distribution.

Typically many thousands, if not tens of thousands, of simulated paths, must be generated to enable an accurate option price to be calculated. When an option is dependent on the underlying assets, then multiple correlated assets paths must be simulated, and the payoff for option premium is discounted.

The options pricing plays an essential role in establishing the value of an option. Option premium pricing provides estimation to the investors to incorporate it into their strategies to maximize profits with MarketXLS. Price movements of the underlying stocks provide insight into the values of options premium.