Managing Your Risk with Option Implied Volatility

Options trading can be an attractive alternative to traditional investments. One of the primary benefits is the ability to manage your risk. However, when trading options, one of the most crucial concepts to understand is implied volatility. This article will provide an overview of Implied Volatility, how it can be used to help you manage your risks, and how MarketXLS can be used as a tool to help traders with their options strategies.

What is Implied Volatility?

Implied Volatility (IV) refers to the volatility that is built into a stock option’s price. It is calculated mathematically from the current market price of an option and the inputs of an option pricing model. This can be used to measure the expected movement of the underlying security against the price of the option.

The most commonly-used option pricing model is the Black-Scholes Model. It requires data inputs such as: the current price of the underlying asset, the strike price of the option, the time to expiration of the option, the risk-free rate, the current implied volatility of the underlying, and the dividend rate of the underlying asset.

What is the Volatility Premium?

The Volatility Premium is the amount that the option is trading for above its intrinsic value. This can happen when the implied volatility of the option is higher than historical volatility of the underlying asset. This is often referred to as a Volatility Smile or Volatility Smirk. It’s important to understand the concept of the Volatility Premium and how it can be used to your advantage when trading options.

What are Option Greeks?

Option Greeks are the risk metrics that are used to measure the sensitivity of the price of an option to changes in certain variables. The most commonly used Option Greeks are Delta, Gamma, Theta, Vega and Rho. Delta measures the rate of change of an option’s price relative to the underlying security’s price. Gamma measures the rate of change of Delta as the underlying security’s price changes. Theta measures the time decay of an option’s value as time passes.

Vega measures the sensitivity of an option’s price to changes in the implied volatility of the underlying security. Lastly, Rho measures the sensitivity of an option’s price to changes in the interest rate. Understanding Option Greeks and how they interact with each other can help you better understand the price dynamics of an option.

What is the VIX Index?

The VIX Index is an index that measures the implied volatility of major US stock indices. It is also known as the “Fear Index” and is often used as a gauge of investor sentiment. The VIX Index can be used to measure the overall level of implied volatility in the markets. This can be a useful tool for investors who want to get an idea of how volatile the markets may be over the short-term or long-term.

What is Volatility Skew?

Volatility Skew is the curvature of the implied volatility surface. It is the difference between implied volatilities at different strike prices. When the skew is positive, the implied volatilities of options with higher strike prices are more expensive than those with lower strike prices. This is known as a Volatility Smirk. When the skew is negative, the implied volatilities of options with higher strike prices are cheaper than those with lower strike prices. This is known as a Volatility Smile.

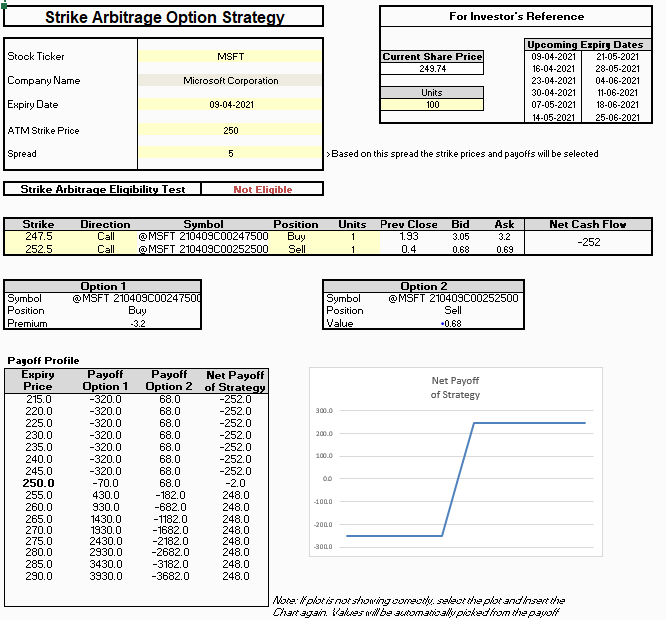

What are Implied Volatility Spreads?

Implied Volatility Spreads are option trades that involve buying and selling options with different strike prices but the same expiration date. They are used to take advantage of the volatility skew and can be used as a way to increase your potential returns. They can also be used as a way to hedge against the downside risk of a position as well.

How Can I Use Implied Volatility to Manage My Risk?

Implied volatility is an important concept to understand when trading options. It can help you understand the current sentiment of the market and how the underlying security could move over the short-term or long-term. It can also be used to help you manage your risks when trading options. You can use implied volatility to select which strategies to employ for a particular underlying stock or ETF.

By understanding the concept of implied volatility and the Option Greeks, you can select strategies that minimize the risks of trading options. You can

Here are some templates that you can use to create your own models

Search for all Templates here: https://marketxls.com/templates/

Relevant blogs that you can read to learn more about the topic

Difference Between Historical And Implied Volatility

Take the Guesswork Out of Options Trading with a Call Option Calculator

Earnings Announcement- It’S Impact On Implied Volatility

Analyze Risk & Reward with a Stock Option Calculator

Long Call Diagonal Spread – An Advance Option Strategy