Introduction

A collar option strategy works as a two-way street to protect the investor against the risk of losses from a fall in the value of an underlying asset. It combines two varied strategies to limit the loss cap and the gain cap simultaneously involved in an investment. The aim of this strategy is not to produce heavy gains but to provide cover against losses. It sums protective put and covered call strategy to make its magic work. Let’s further take an in-depth analysis of the collar options strategy as below.

Protective put strategy

The protective put strategy is also known as a synthetic call, it involves managing the underlying risk against an asset by buying an option at a strike price almost near or equal to the current market value of the asset. It aims at holding a long position against the asset and provides protection in cases of a decrease in the market value.

Covered call strategy

The covered call strategy provides a cover along with the protective put to exercise the collar options strategy. It involves typically selling an OTM (out of the money) call option when the strike price is higher than the market price of an asset.

How does the collar option work?

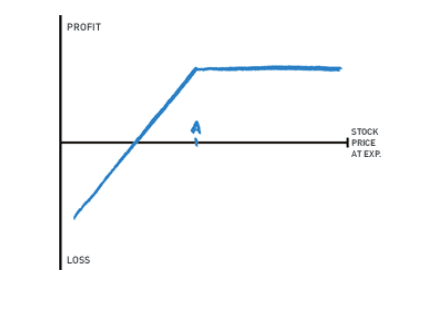

The collar option strategy is created when a long underlying asset is purchased along with a long OTM put option and a short OTM call option. The investor enjoys profit because of its long position on the underlying asset when its price increases in the market and vice versa faces loss when the price falls down but in the latter case holding the long position on the OTM put option provides cover against the decrease in the asset value and the put option value increases. Hence, it neutralizes the overall impact of the trade. In a similar manner, when there is an increase in the value of the underlying asset, the investor can experience losses due to his short position on an OTM call position. This potential loss neutralizes the upside of holding the stock.

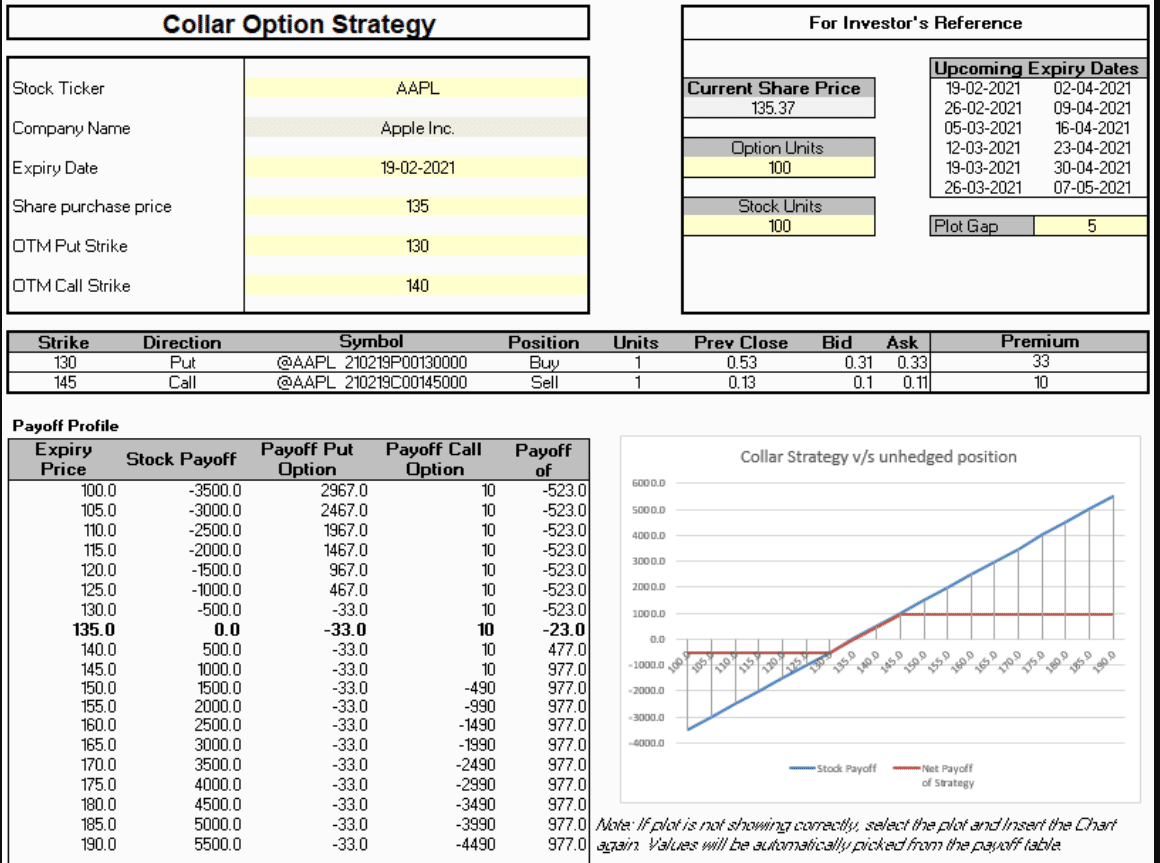

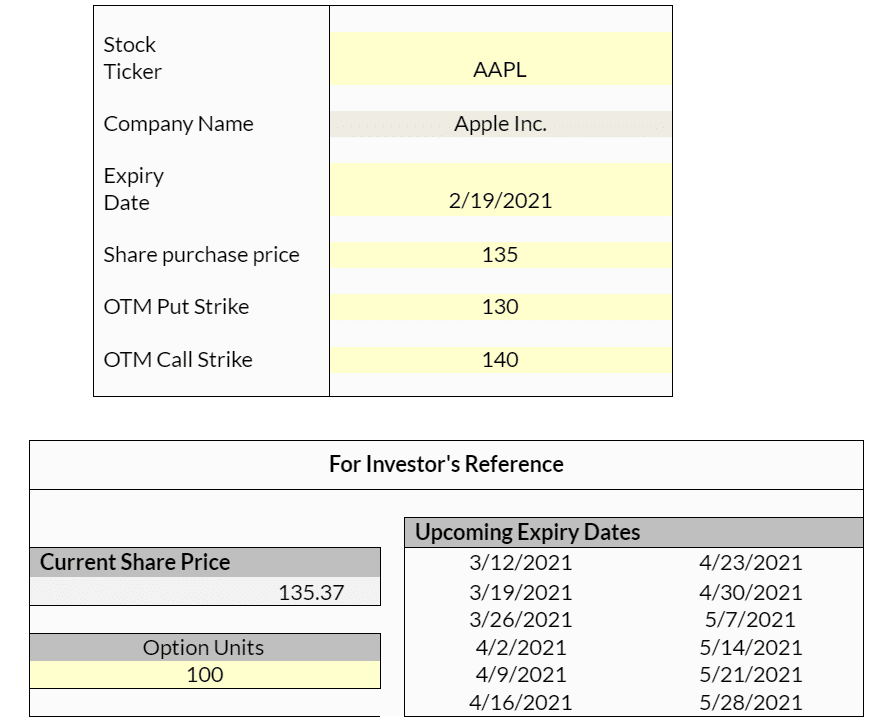

Working with MarketXLS template

Let’s work out an example for collar option strategy with MarketXLS template,

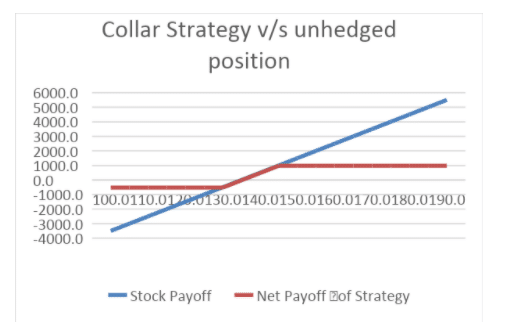

Suppose an investor purchased certain shares of the XYZ stock currently priced at $100. To utilize the collar options strategy, he holds a long position on the asset and buys a put option with a strike price of $90 and a premium of $5 and sells a call option with a strike price of $110 values at $5. The payoff in case of a fall in the value (from $100 to $80) of the underlying asset will result in using the put option with its original values while the call option will become pointless with a payoff of $5. Considering the total original loss of $20 ($100 – $80), the covered call strategy will bring the net loss to a value of $10 ($5+$5-$20). Therefore hedging the losses involved in the investment because of the protective put.

Similarly, in case of an increase (from $100 to $115) in the value of the same asset will result in exercising the use of the call option at the agreed strike price and the payoff against it will become zero. The put option purchased will become pointless and the original gains ($115 – $100 = $15) attained will net the payoff to a total of $10 ($0-$5+$15 = $10). Hence, the collar option capped the upside potential of the trade-in attaining higher gains.

Uses

A collar option strategy is utilized by any investor in order to control the impact of the risk in case of a bullish prediction for the market. It functions as a flexible hedging option. The protective put provides coverage in case of a fall in price and the covered call does the same in case of an increase in the market value of the asset. In a stock deal, a collar can be used to ensure that a potential depreciation of the acquirer’s stock does not lead to a situation where they must pay much more in diluted shares. The net cash flow will be very small (can be negative) as the aim of this strategy is not to benefit from selling options but to protect the downside of the stock price.

Disclaimer

None of the content published on marketxls.com constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The author is not offering any professional advice of any kind. The reader should consult a professional financial advisor to determine their suitability for any strategies discussed herein. The article is written for helping users collect the required information from various sources deemed to be an authority in their content. The trademarks if any are the property of their owners and no representations are made.

References

https://corporatefinanceinstitute.com/